Accounting – How to Prepare a Company’s First Bank Reconciliation Statement

A bank reconciliation statement is an important tool when it comes to managing your company’s cash flow. It can help you to verify that your bank account ending balance as indicated in the bank statement matches the bank balance indicated in your general ledger. The preparation of the bank reconciliation statement involves making adjustments to the bank balance your company books and the bank statement to ensure that every item is accounted for and the balances match (Also see Accounting for Book and Bank Overdrafts and their Cash Flow). This is crucial control in an effort to ensure the accuracy of the accounts.

If you are preparing a bank reconciliation statement for a business that has never prepared one, follow these steps.

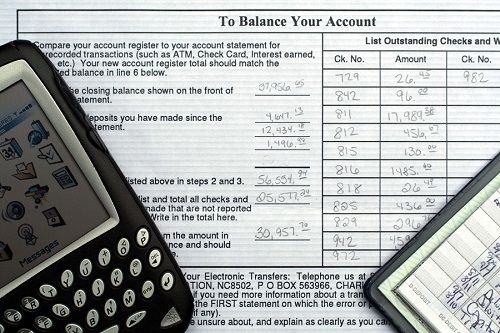

Step 1: Make a list of all outstanding cheques

Use the bank statement to know the outstanding cheques. For instance, if the bank statement is dated 31st August, look at the bank statements that were released from June to August and write down the cheque numbers that were written after 1st June but didn’t feature on any bank statement from June to August.

Record the amount for each cheque and sum up the amounts. Then, subtract the total amount of outstanding cheques as of 31st August from the bank balance indicated in the bank statement date 31st August. The resulting amount is known as the adjusted balance per bank.

Step 2: Compare the general ledger account and the bank statement

In this step, use the general ledger account that is directly related to the bank statement. In this case, let’s assume it’s a cash in bank account. You must be sure that the cash account has items that also appear in the bank statements released recently.

Find out if the bank service charges, electronic transfers, and other transactions that are shown in the bank statements are entered in the cash in bank account. Also, record the same amount in the income statement account. If you notice that some entries are missing from the cash account, include them instead. You may also need to check earlier bank statements to ensure that every entry in the bank statement is reflected in the cash in bank account.

Eventually, you must ensure that the cash in bank account balance is equal to the adjusted balance (Also see What are Correcting Entries?) per bank that you calculated in step 1. If these two balances are different, then it is likely that the step 1 and 2 wasn’t being carried out properly and you might want to re-do the flow. Maintain a copy of your documentation and open a file titled “Bank Reconciliations”. The accounting services we provided included this reconciliation feature and ensure things are always under control.